True/False

Indicate whether the

sentence or statement is true or false.

|

|

|

1.

|

Total revenue equals the quantity of output the

firm produces times the price at which it sells its output.

|

|

|

2.

|

Wages and salaries paid to workers are an example

of implicit costs of production.

|

|

|

3.

|

If total revenue is €100, explicit costs are

€50, and implicit costs are €30, then accounting profit equals €50.

|

|

|

4.

|

If there are implicit costs of production,

accounting profits will exceed economic profits.

|

|

|

5.

|

When a production function gets flatter, the

marginal product is increasing.

|

|

|

6.

|

If a firm continues to employ more workers within

the same size factory, it will eventually experience diminishing marginal product

|

|

|

7.

|

If the production function for a firm exhibits

diminishing marginal product, the corresponding total cost curve for the firm will become flatter as

the quantity of output expands.

|

|

|

8.

|

Fixed costs plus variable costs equal total

costs.

|

|

|

9.

|

Average total costs are total costs divided by

marginal costs.

|

|

|

10.

|

When marginal costs are below average total costs,

average total costs must be falling.

|

|

|

11.

|

If, as the quantity produced increases, a

production function first exhibits increasing marginal product and later diminishing marginal

product, the corresponding marginal cost curve will be U-shaped.

|

|

|

12.

|

The average total cost curve crosses the marginal

cost curve at the minimum of the marginal cost curve.

|

|

|

13.

|

The average total cost curve in the long run is

flatter than the average total cost curve in the short run.

|

|

|

14.

|

The efficient scale for a firm is the quantity of

output that minimizes marginal cost.

|

|

|

15.

|

In the long run, as a firm expands its production

facilities, it generally first experiences diseconomies of scale, then constant returns to scale, and

finally economies of scale.

|

Multiple Choice

Identify the

letter of the choice that best completes the statement or answers the question.

|

|

|

16.

|

Accounting profit is equal to total revenue

minus

a. | implicit costs. | b. | variable costs. | c. | the sum of

implicit and explicit costs. | d. | explicit

costs. | e. | marginal costs. |

|

|

|

17.

|

Economic profit is equal to total revenue

minus

a. | variable costs. | b. | implicit costs. | c. | explicit

costs. | d. | marginal costs. |

|

|

|

18.

|

Nicole owns a small pottery factory. She can make

1,000 pieces of pottery per year and sell them for €100 each. It costs Nicole €20,000 for

the raw materials to produce the 1,000 pieces of pottery. She has invested €100,000 in her

factory and equipment: €50,000 from her savings and €50,000 borrowed at 10 per cent.

(Assume that she could have loaned her money out at 10 per cent, too.) Nicole can work at a competing

pottery factory for €40,000 per year. The accounting profit at Nicole's pottery factory

is

a. | €30,000. | b. | €35,000. | c. | €75,000. | d. | €70,000. | e. | €80,000. |

|

|

|

19.

|

Nicole owns a small pottery factory. She can make

1,000 pieces of pottery per year and sell them for €100 each. It costs Nicole €20,000 for

the raw materials to produce the 1,000 pieces of pottery. She has invested €100,000 in her

factory and equipment: €50,000 from her savings and €50,000 borrowed at 10 percent

(assume that she could have loaned her money out at 10 percent, too). Nicole can work at a competing

pottery factory for €40,000 per year. The economic profit at Nicole's pottery factory

is

a. | €80,000. | b. | €30,000. | c. | €75,000. | d. | €70,000. | e. | €35,000. |

|

|

|

20.

|

If there are implicit costs of

production,

a. | accounting profit will exceed economic

profit. | b. | economic profit will always be

zero. | c. | economic profit will exceed accounting

profit. | d. | accounting profit will always be

zero. | e. | economic profit and accounting profit will be

equal. |

|

|

|

21.

|

If a production function exhibits diminishing

marginal product, its slope

a. | is linear (a straight line). | b. | becomes steeper as the quantity of the input

increases. | c. | could be any of

these answers. | d. | becomes flatter as

the quantity of the input increases. |

|

|

|

22.

|

If a production function exhibits diminishing

marginal product, the slope of the corresponding total-cost curve

a. | is linear (a straight line). | b. | could be any of these answers. | c. | becomes steeper as the quantity of output

increases. | d. | becomes flatter as

the quantity of output increases. |

|

|

|

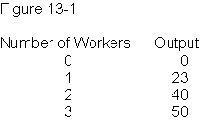

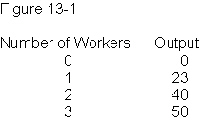

23.

|

Refer to Figure 13-1. The marginal product of

labour as production moves from employing one worker to employing two workers is

|

|

|

24.

|

Refer to Figure 13-1. The production process

described above exhibits

a. | constant marginal product of

labour. | b. | diminishing marginal product of

labour. | c. | increasing returns to scale. | d. | increasing marginal product of labour. | e. | decreasing returns to scale. |

|

|

|

25.

|

Which of the following is a variable cost in the

short run?

a. | rent on the factory | b. | wages paid to factory labour | c. | interest payments on borrowed financial capital | d. | payment on the lease for factory equipment | e. | salaries paid to upper management |

|

|

|

26.

|

Refer to Figure 13-2. The average fixed cost of

producing four units is

| Figure 13-2 | | | Quantity of Output | Fixed

Costs | Variable Costs | Total Costs | Marginal

Costs | 0 | €10 | €0 | | | | | | | | | 1 | 10 | 5 | | | | | | | | | 2 | 10 | 11 | | | | | | | | | 3 | 10 | 18 | | | | | | | | | 4 | 10 | 26 | | | | | | | | | 5 | 10 | 36 | | | | | | | |

a. | €2.50. | b. | €26. | c. | none of these

answers. | d. | €10. | e. | €5. |

|

|

|

27.

|

Refer to Figure 13-2. The average total cost of

producing three units is| Figure 13-2 | | | Quantity of Output | Fixed

Costs | Variable Costs | Total Costs | Marginal

Costs | 0 | €10 | €0 | | | | | | | | | 1 | 10 | 5 | | | | | | | | | 2 | 10 | 11 | | | | | | | | | 3 | 10 | 18 | | | | | | | | | 4 | 10 | 26 | | | | | | | | | 5 | 10 | 36 | | | | | | | |

a. | €28. | b. | €6. | c. | €3.33. | d. | €18. | e. | €9.33. |

|

|

|

28.

|

Refer to Figure 13-2. The marginal cost of changing

production from three units to four units is| Figure

13-2 | | | Quantity of Output | Fixed Costs | Variable

Costs | Total Costs | Marginal Costs | 0 | €10 | €0 | | | | | | | | | 1 | 10 | 5 | | | | | | | | | 2 | 10 | 11 | | | | | | | | | 3 | 10 | 18 | | | | | | | | | 4 | 10 | 26 | | | | | | | | | 5 | 10 | 36 | | | | | | | |

a. | €7. | b. | €5. | c. | €8. | d. | €9. | e. | €6. |

|

|

|

29.

|

Refer to Figure 13-2. The efficient scale of

production is| Figure 13-2 | | | Quantity of

Output | Fixed Costs | Variable Costs | Total

Costs | Marginal Costs | 0 | €10 | €0 | | | | | | | | | 1 | 10 | 5 | | | | | | | | | 2 | 10 | 11 | | | | | | | | | 3 | 10 | 18 | | | | | | | | | 4 | 10 | 26 | | | | | | | | | 5 | 10 | 36 | | | | | | | |

a. | two units. | b. | three units. | c. | one

unit. | d. | five units. | e. | four units. |

|

|

|

30.

|

When marginal costs are below average total

costs,

a. | average fixed costs are

rising. | b. | average total costs are

falling. | c. | average total costs are

rising. | d. | average total costs are

minimized. |

|

|

|

31.

|

If marginal costs equal average total

costs,

a. | average total costs are

falling. | b. | average total costs are

rising. | c. | average total costs are

maximized. | d. | average total

costs are minimized. |

|

|

|

32.

|

If, as the quantity produced increases, a

production function first exhibits increasing marginal product and later diminishing marginal

product, the corresponding marginal-cost curve will

a. | be flat (horizontal). | b. | slope upward. | c. | slope

downward. | d. | be U-shaped. |

|

|

|

33.

|

In the long run, if a very small factory were to

expand its scale of operations, it is likely that it would initially experience

a. | an increase in average total

costs. | b. | diseconomies of scale. | c. | economies of scale. | d. | constant returns

to scale. |

|

|

|

34.

|

The efficient scale of production is the quantity

of output that minimizes

a. | average fixed cost. | b. | average total cost. | c. | average variable

cost. | d. | marginal cost. |

|

|

|

35.

|

Which of the following statements is

true?

a. | All costs are fixed in the short

run. | b. | All costs are variable in the long

run. | c. | All costs are variable in the short

run. | d. | All costs are fixed in the long

run. |

|